The price of crude oil extended the losses for three successive weeks, following the linear fate of LNG, liquified natural gas, which fell by over 40% in June, having reached the highest at $9.33.

As of 09:45 GMT, the prices of WTI, Brent and LNG stood at $106.37, $109.90 and $5.72 respectively.

The lingering fear of a major global recession weighs heavily on the current sentiments in the energy markets; the obvious supply-side woes have not been able to push the prices up steadily in the recent weeks, defying the pundits.

The OPEC+, meanwhile, reiterated its commitment to increase the production by 648,000 bpd for July and August in their latest monthly meeting on Thursday. The cartel, however, did not say about their plans beyond August, implying the anxiety of the members over the demand in the coming months.

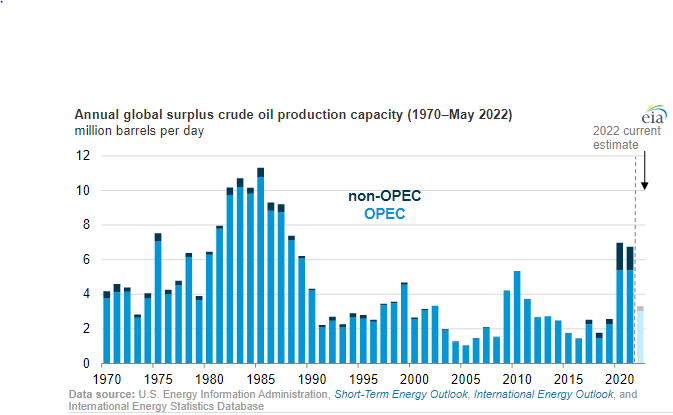

Although analysts intensely focus on the US crude inventory data that is available on weekly basis from two major sources, the EIA, US Energy Information Administration, sheds light on yet another factor that is often overlooked - global surplus crude oil production capacity.

The EIA defines the surplus production capacity as the maximum capacity that can be brought online in 30 days and sustained for at least 90 days.

Compared with the figure in May 2021, the EIA says, the surplus production capacity of the non-OPEC members has plunged by 80%: it is a drop from 1.4 million bpd to a mere 280,000 bpd, 60% of which is in Russia.

These estimates, however, do not include the crude oil volumes that are offline due to unexpected outages and sanctions - in line with the definition; they simply cannot be brought online in a rush and such a prospect is unrealistic, despite the demand being high.

As for the OPEC, according to the EIA, the surplus production capacity has gone down from 5.4 million bpd in May 2021 to 3 million bpd in May 2022.

In this context, the grievances expressed by the major oil producers in the Middle East, confirmed from the lip reading of President Macron to President Biden while in a whisper, are understandable; the former are making a point, indeed.

In short, the global crude surplus production capacity in 2022 is less than half of the same in 2021.

Since there is no sign of a let-up in the war between Russia and Ukraine, it is highly unlikely that the sanctions against the former will be lifted anytime soon, leaving Russia's vast surplus production capacity untapped for months, if not years, to come; for the same reason, the collective contribution of Iran and Venezuela will remain in the doldrums for the foreseeable future too.

The political rivalries among the current Libyan rulers do not make the Libyan contribution on the same front feasible either - any time soon.

All in all, it is highly unlikely that the oil prices will go below $100 a barrel in the coming months; even if it goes downhill on account of negative market sentiments, metaphorically speaking, there is plenty of upthrust in the form of supply constraints to keep it floating above the crucial - and damaging - current three-digit mark.